But that shouldn’t stop you from buying that bag you’ve been eyeing, the pair of shoes sitting in your cart, or anything else you were ready to check out with. The idea behind splitting payments is convenience, and if one app can’t support that purchase, there are plenty of others that can.

And that’s exactly why we’re here. In this guide, we’ll walk you through some of the best Sezzle alternatives that can give you the same pay-later flexibility, sometimes with higher limits, wider store acceptance, or features that make checkout a lot smoother. So, let’s begin!

A Quick Glance at the Best Apps Like Sezzle on Our List

We’ve rounded up the top 6 apps that offer similar pay-later flexibility as Sezzle. So, before we dive into each one, here’s a quick overview.

| Name of the App | Best For | Spending Limit | Key Differentiator |

|---|---|---|---|

| Klarna | Shoppers who want flexibility with various payment plans and potential rewards | No predefined limit. (Dynamically assessed based on purchase power; no hard minimum/maximum) | Integrated shopping browser and the Klarna Rewards program |

| Affirm | Users looking for longer-term financing for larger purchases, with fixed interest rates | $50 minimum; up to $20,000 maximum (can reach up to $30,000 with select merchants like Amazon) | Focuses heavily on larger purchases with transparent, simple interest loans and absolutely zero late fees |

| Afterpay | Consumers who want straightforward Pay in 4 options with no additional interest | Up to $4,000 maximum. (New accounts typically start with a strict limit of around $600) | Widespread popularity and deep integration, especially in the US fashion and beauty sectors |

| PayPal | Existing PayPal users who appreciate the convenience of an all-in-one app | Pay in 4: $30–$1,500 Pay Monthly: $49–$10,000 (requires a minimum purchase of $199) |

Leverages the trusted PayPal ecosystem and extensive US merchant network |

| Zip | Users who need greater flexibility for using BNPL, even at stores that don't directly offer it | $35 minimum; up to $1,500 maximum | The app allows you to generate a virtual card to use BNPL almost anywhere Visa is accepted |

| Zilch | UK users seeking flexibility and potential cashback rewards | Generally dynamic and dependent on individual credit assessment | Offers cashback on purchases and has a virtual card for wider acceptance |

Read Less

List of the Best Apps Like Sezzle

Pros & Cons

Pros

- You can generate a one-time virtual card to shop at almost any online retailer

- The app offers multiple payment options, including Pay in 4, Pay in 30 days, and monthly financing

- You can earn cashback rewards and access exclusive deals directly within the app

- It includes a built-in package tracker that monitors all your deliveries in one place

- The app lets you store digital loyalty cards for easy access during checkout

Cons

- Using a one-time virtual card at non-partner stores often incurs a service fee

- Your available spending limit fluctuates constantly based on real-time soft credit checks

- Having multiple active payment plans simultaneously makes it easy to overspend

Why You'll Love It

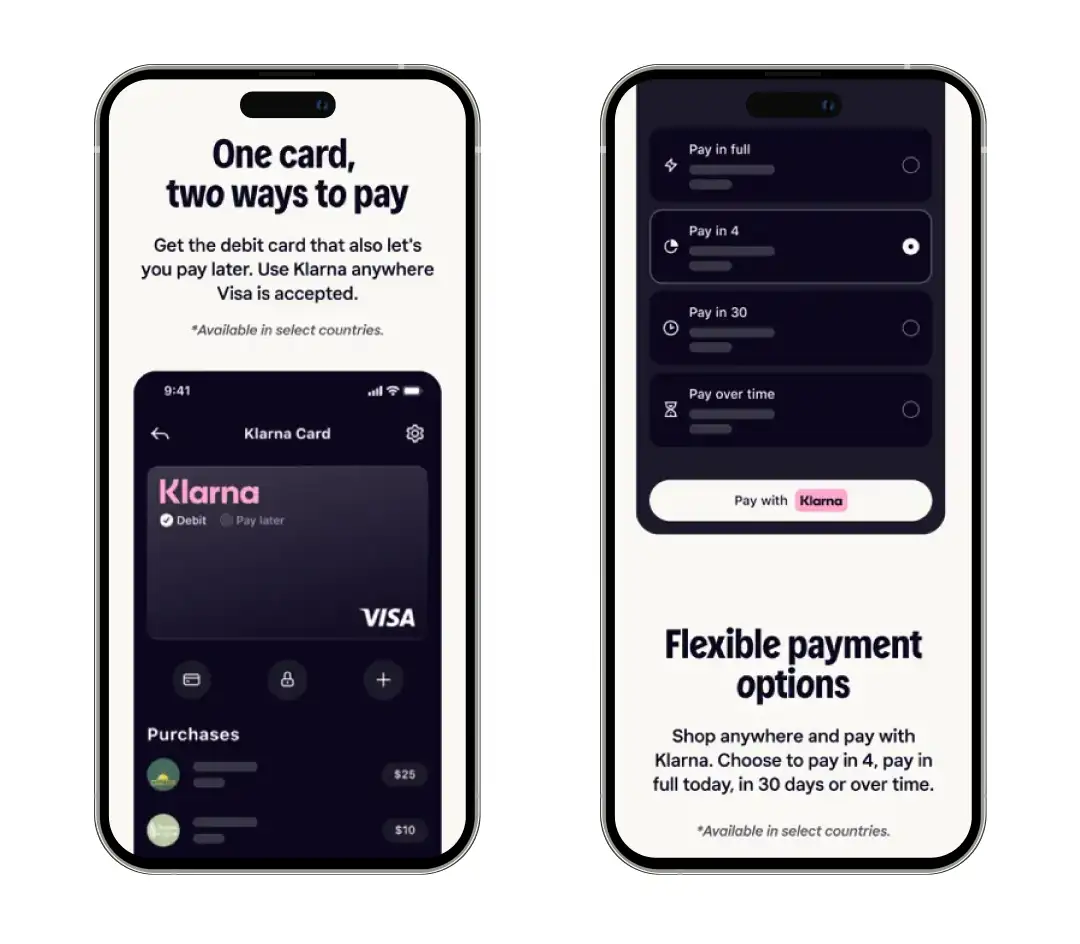

Along with offering basic split payments like Sezzle, Klarna doubles as a robust rewards hub that actually pays you to shop, letting you earn up to 10% cashback at major retailers like Amazon and Walmart. Plus, its native Apple Pay integration allows you to split payments directly from your iPhone's digital wallet in physical stores.More about product

While researching for safe and legit apps like Sezzle, our team was particularly impressed by Klarna. We think it tops the list because it builds a highly comprehensive financial ecosystem. Unlike its competitors, Klarna guarantees zero hidden fees for on-time payments.

It seamlessly connects with both Apple Pay and Google Pay, and even offers a physical Visa card, allowing you to split costs in-store at major retailers like Walmart, Nike, and Target. Beyond mobile, its robust browser extension brings this same flexibility directly to your desktop shopping.

The platform also excels as a personal finance manager, featuring intuitive spending and balance tracking tools that keep your budget in check. By merging in-store integrations and transparent fee structures, Klarna delivers a remarkably secure shopping experience everywhere!

Pros & Cons

Pros

- Strictly promises never to charge any late fees, hidden fees, or prepayment penalties

- You can finance much larger purchases with repayment terms extending up to 3, 6, 12months or more

- Uses simple interest, so your total amount owed never unexpectedly increases

- Features a high-yield savings account to help your money grow

- The Affirm Card lets you link your bank account and request payment splits

Cons

- Financing longer-term or high-ticket items may require a hard credit check that impacts your score

- The interest rates for extended payment plans can reach up to 36% APR, depending on your credit

- Lacks the comprehensive, gamified shopping browser and cashback rewards ecosystem found in competing apps

Why You'll Love It

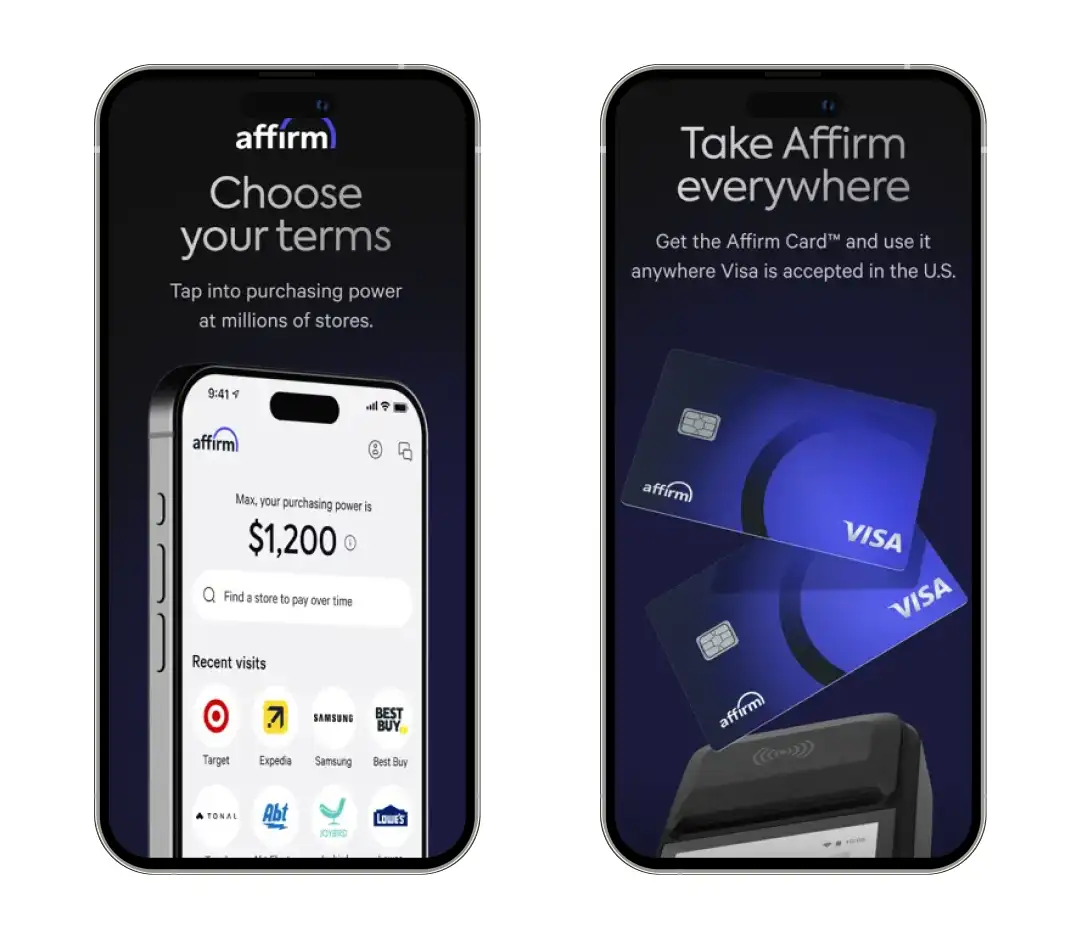

Affirm is the undisputed king of financing major life expenses. You'll love their ironclad no late fees ever guarantee and the ability to stretch payments for big-ticket items like furniture or vacations out to 36 months.More about product

If you are looking to finance substantial purchases, Affirm is an absolute powerhouse. This app completely redefines how users manage larger expenses. Unlike other payment apps like Sezzle, which are focused mostly on short-term installments, Affirm allows you to finance up to $20,000 with repayment terms extending up to five years.

You still get interest-free options like ‘Pay in 4,’ but its monthly financing uses simple interest with a strict no-fee policy, guaranteeing absolutely no late penalties. Boasting direct integrations with retail giants like Amazon and Costco, the app makes checkout a breeze.

You can also use the physical Affirm Card to make direct payments to the stores. Affirm also offers seamless digital wallet compatibility that lets you take your purchasing power anywhere Visa is accepted. You can do it all without ever impacting your credit score.

Pros & Cons

Pros

- The standard Pay in 4 model is always completely interest-free

- It features seamless integration with Cash App, so you can manage your installments easily

- You can clearly view your estimated spend limits upfront before you attempt to check out

- The app allows you to easily reschedule one payment per order if you need a few extra days

- It automatically freezes your account if you miss a payment to prevent debt from snowballing

Cons

- You will be charged late fees of up to $8 if you miss a scheduled payment

- New users are typically restricted to very low initial spending limits

- Longer-term monthly financing options can come with interest rates up to 35.99% APR

Why You'll Love It

Afterpay can be one of the best Sezzle alternatives if you are already an active Cash App user. Because Afterpay is owned by Block, you can manage your buy now, pay later installments directly within your Cash App ecosystem alongside your peer-to-peer transfers and everyday banking.More about product

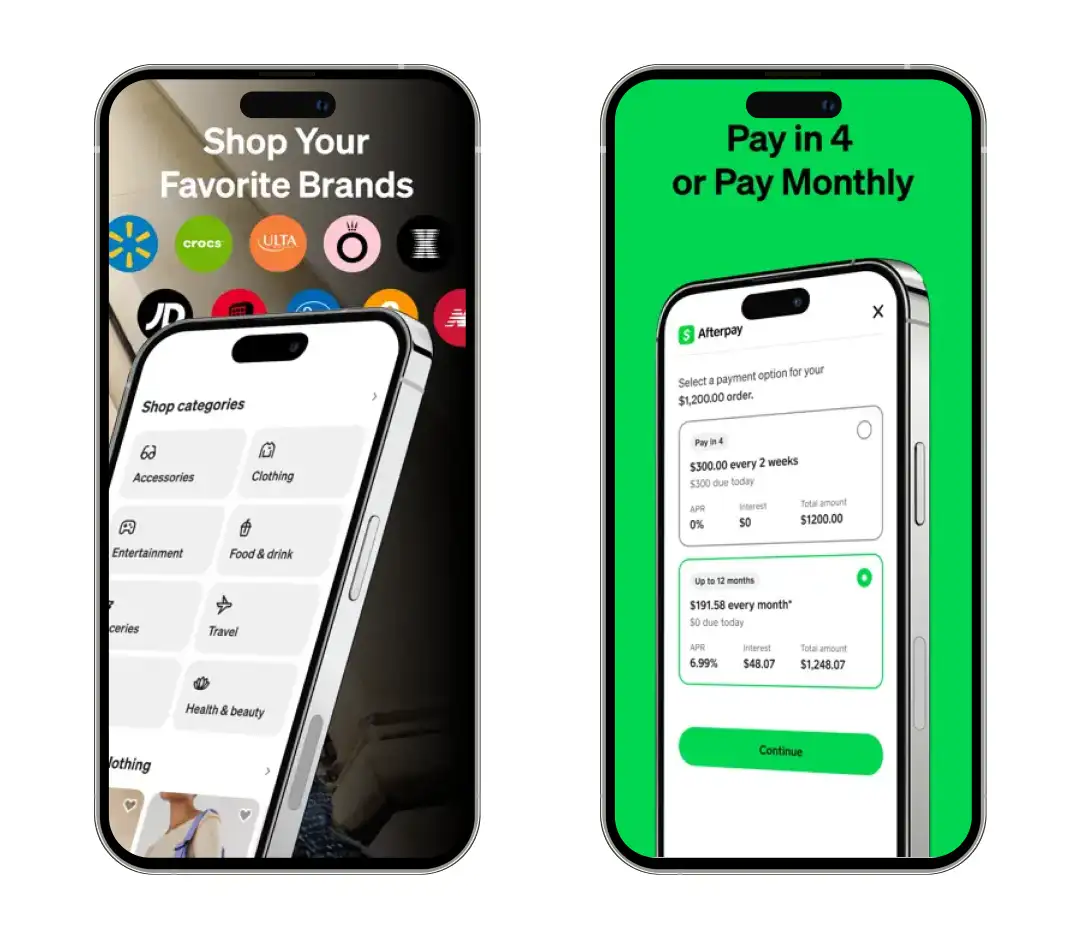

Afterpay uniquely merges smart budgeting with trend discovery; the platform acts as a curated engine featuring editor-picked fashion roundups and app-exclusive deals for fashion, tech, and travel.

It now offers extended monthly financing for up to 24 months to make big-ticket items manageable. It even allows you to finance digital gift cards from top brands to send instantly.

To encourage responsible spending, Afterpay rewards on-time payments with dynamic spending limit increases. It also utilizes a strict smart-pause system that freezes purchasing power if a deadline is missed.

Furthermore, you can customize your payment dates to align with your paychecks. Finally, Afterpay’s fresh, deep integration with Cash App provides unparalleled financial control. This allows you to track deliveries, manage budgets, and ‘Tap to Pay’ securely in-store.

Not Sold on Afterpay? Here are 10 Afterpay Alternatives to Consider

Pros & Cons

Pros

- It is seamlessly integrated into millions of online checkouts

- PayPal strictly does not charge any late fees if you miss a payment

- You can conveniently use your existing PayPal account balance to fund your installment payments

- Purchases made with their BNPL service are fully backed by PayPal's Purchase Protection

- It consolidates your BNPL plans, peer-to-peer transfers, and everyday banking into one platform

Cons

- You must have an active PayPal account in good standing to access their buy now, pay later features

- The approval process is dynamic per transaction, meaning checkout success is never guaranteed beforehand

Why You'll Love It

PayPal is an active, global arbitrator that controls both the buyer's and the seller's accounts on their network. So, if a merchant wrongs you, PayPal can freeze the seller's funds and refund you directly. This gives you unparalleled leverage and consumer power anywhere on the internet.More about product

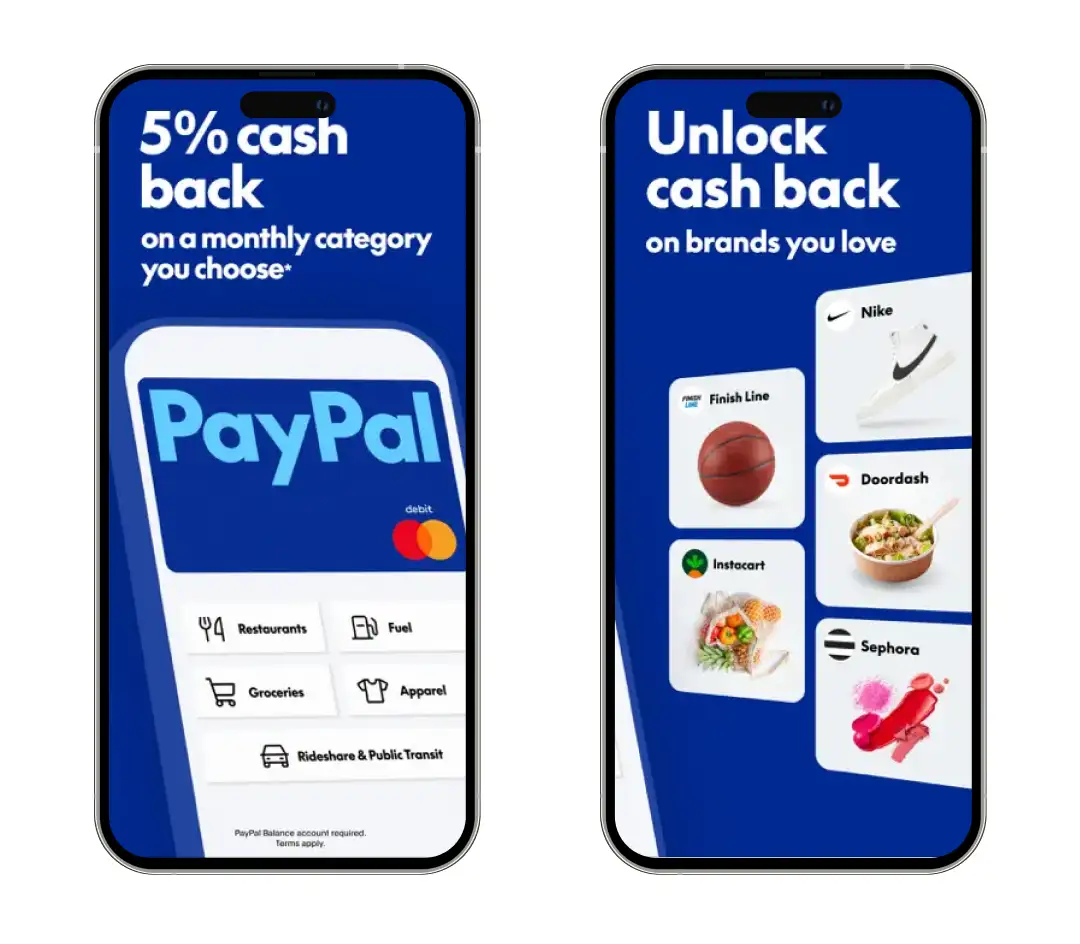

When exploring flexible payment apps like Sezzle, PayPal stood out for us, simply because it does not offer the standard, run-of-the-mill payment splits you see everywhere else. PayPal fundamentally upgrades your purchasing power with two distinct options: a zero-interest ‘Pay in 4’ plan, and an ultra-flexible ‘Pay Monthly’ option.

This allows you to conquer massive purchases by spreading costs seamlessly across up to 24 months with zero sign-up fees. Along with being a trusted digital payment app in the USA, what truly makes this app a great Sezzle alternative is its colossal, all-in-one wealth and shopping ecosystem.

It automatically hunts down and applies exclusive brand rewards directly at checkout, and lets you earn up to 5% cash back on tailored categories using its Debit Mastercard. It seamlessly blends this heavy-hitting financing with ingenious lifestyle features, like built-in package tracking that links straight to your Gmail or Outlook, instant global money transfers, and even cryptocurrency trading.

PayPal isn't just an app for dividing a bill; it is the ultimate, battle-tested financial hub for users who demand absolute control, ironclad security, and maximum rewards every single time they click buy.

Pros & Cons

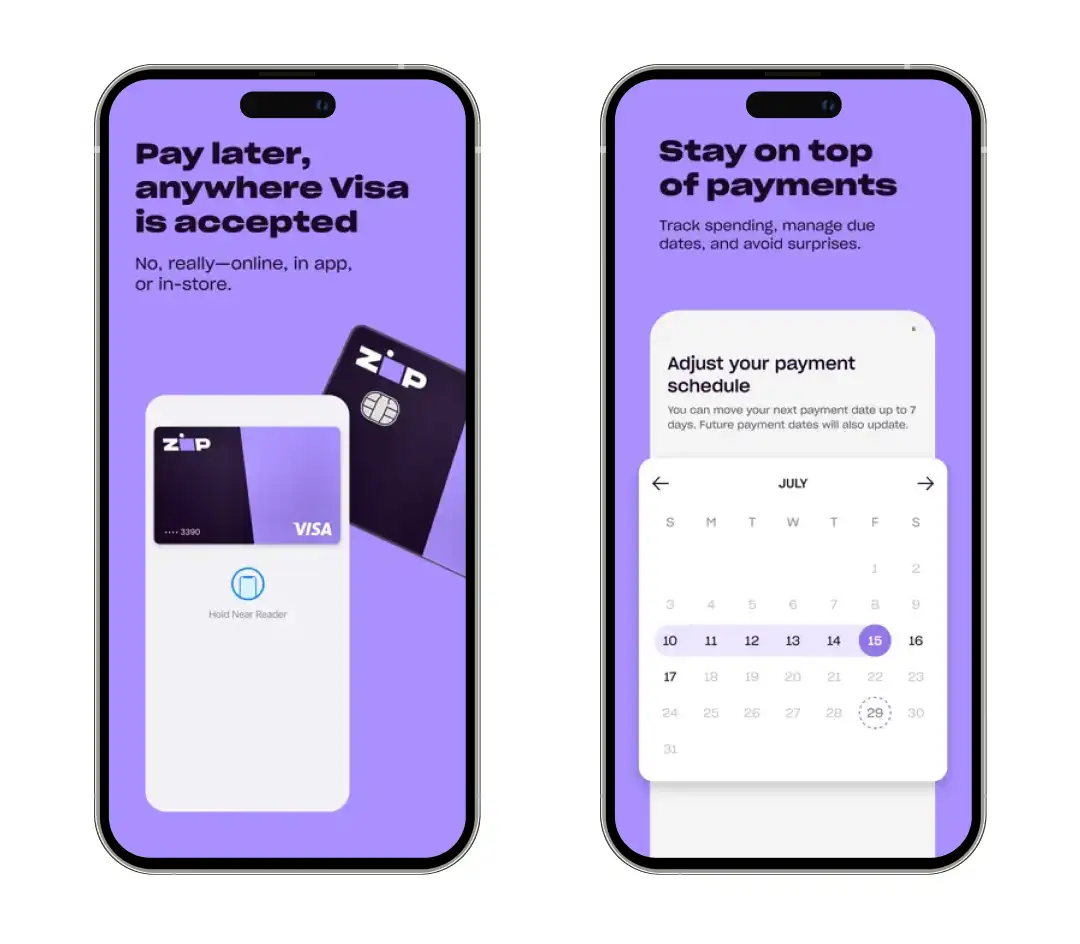

Pros

- You can generate a single-use virtual Visa card to split payments at virtually any retailer that accepts Visa

- Offers highly flexible terms, allowing you to split purchases into 2, 4, or 8 bi-weekly installments

- The app gives you the rare ability to reschedule a payment date to better align with your actual payday

- Zip offers both a physical card and seamless integration with Apple Pay and Google Pay

- Applying for an account and checking your spending power only requires a soft credit check

Cons

- Zip is not entirely free to use. They charge an upfront origination/installment fee, ranging from $4 to over $62

- Despite the feeling of borderless freedom, Zip strictly limits its app, virtual cards, and physical cards to U.S. domestic purchases only

- Missing a payment will result in late fees and will immediately lock your account from making future purchases

Why You'll Love It

Zip's unique selling proposition is its unrestricted retail freedom, achieved through a browser-based shopping model that bypasses the need for merchant partnerships. It effectively turns every physical store with a tap-to-pay terminal into a buy-now-pay-later merchant, giving you total control over your cash flow.More about product

While most apps restrict you to a specific list of partners, Zip’s ‘Pay Anywhere’ technology generates a unique virtual card on the fly, allowing you to split everything from your morning grocery haul and monthly utility bills to emergency car repairs into manageable bites.

If you are someone seeking complete freedom to shop from anywhere, this app is designed for you. It offers unparalleled flexibility with options to pay in 4 or 8 installments, plus the rare ability to shift your payment dates to match your actual payday.

With its sleek interface and a physical Zip Card for seamless in-store use, Zip is a master key that unlocks everyday convenience. This app truly shatters the boundaries of traditional shopping by giving you the freedom to pay in installments almost anywhere Visa is accepted, even at retailers that don’t officially offer BNPL.

Pros & Cons

Pros

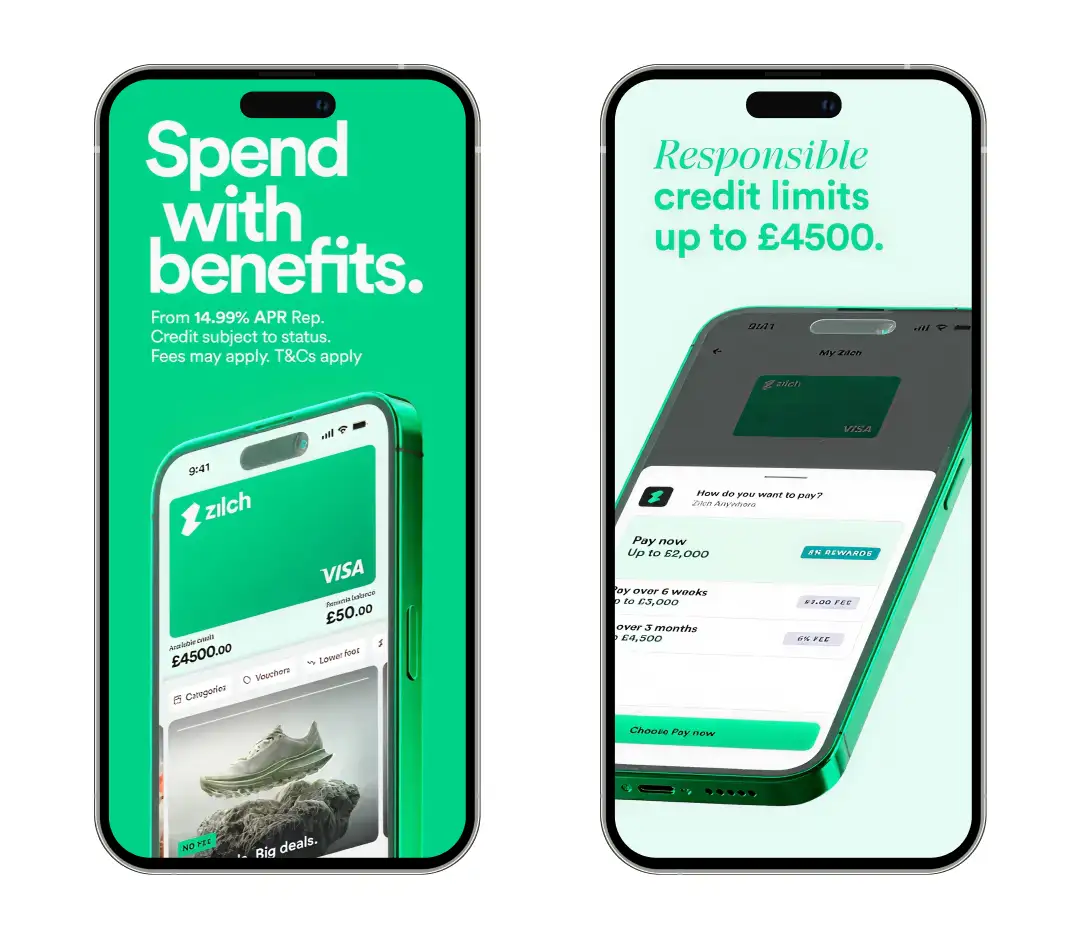

- You can split purchases over 6 weeks or 3 months with zero interest and zero fees

- If you have the cash, you can pay in full immediately and earn Zilch Rewards

- Zilch reports your on-time payments to major UK credit bureaus, actively helping you build your credit score

- Applying for an account only requires a soft credit pull, meaning simply checking your eligibility

- The virtual Mastercard integrates seamlessly with Apple Pay, Google Pay, and Samsung Pay

Cons

- Pushing back a payment using the ‘Snooze feature will cost you a small fee

- Because they report to credit bureaus, failing to make your payments on time will negatively impact your traditional credit score

- Missing a scheduled payment will immediately lock your account, preventing you from making new purchases

Why You'll Love It

While most BNPL apps only offer pay-later options, Zilch is a rare hybrid that rewards you for responsible spending and helps you grow your credit score. Its ‘Pay in 1’ feature gives you instant cashback for paying upfront. The bonus? As they report to all three major bureaus, your on-time payments actually work toward your long-term financial health.More about product

While researching how Zilch is a better alternative to Sezzle, we noticed that it behaves more like a smart credit card than a simple installment app. Its standout feature is the integration of Open Banking, which looks at your real-time income and expenses to set a personalized spending limit that prevents you from overextending yourself.

While using the app, the ‘Zilch Anywhere’ function provides a level of freedom most competitors can't match, allowing you to use your virtual or physical Mastercard at virtually any retailer worldwide. Though it's worth noting that splitting payments this way incurs a small fixed fee, and international purchases are subject to standard foreign exchange fees.

If you find yourself in a tight spot, their ‘Snooze’ button offers a stress-free way to push back an installment by 4 or 8 days for a nominal fee (starting at £0.75), avoiding the fear of predatory late penalties.

Most uniquely, Zilch flips the script on traditional BNPL by offering a ‘Pay Now’ option. If you have the cash, you pay in full and get a chunk of it back in rewards to use on your next purchase.

*Please note, however, that Zilch is currently largely available to UK users only.

How Did We Pick the Best Buy Now, Pay Later Apps Like Sezzle For Our List

To ensure we provide you with a reliable and high-quality selection of Buy Now, Pay Later (BNPL) apps like Sezzle, we rely on a rigorous, data-driven methodology. Our ranking process is built on a foundation of deep industry expertise and hands-on testing.

We don't just aggregate opinions; our dedicated internal team of tech analysts personally interacts with / researches each app to evaluate its real-time performance, security protocols, and feature utility.

By combining proprietary scoring algorithms with verified user feedback and strict vetting criteria, such as compliance with financial standards and UI/UX intuitiveness, we transform complex data into clear, authoritative rankings.

This methodical approach ensures that every app we recommend is not only a market leader but a secure and practical solution for your financial needs.

How Can You Choose the Best Sezzle Alternatives

While Sezzle is a fan-favorite for its user-friendly interface and easy payment models, it may not always be the perfect fit for your specific shopping habits or financial goals. To find the right alternative, you need to look beyond the surface and evaluate how a platform aligns with your budget and lifestyle.

Here are the key factors to consider when choosing the best Sezzle alternative:

Key Factor What to Look For Repayment Flexibility and Terms Choose between standard ‘Pay-in-4’ plans or extended monthly terms (up to 48 months) based on the size of your purchase Fee Transparency and Interest Rates Check the fine print for late fees, rescheduling penalties, and long-term APRs, even if they advertise 0% interest Merchant Compatibility Ensure the app is accepted at your favorite stores, or look for virtual cards that allow for universal checkout Credit Reporting and Impact Decide if you want soft credit checks that hide your activity, or opt-in reporting to actively build your credit score Approval Odds and Spending Limits Look for instant approvals and dynamic spending limits that increase as you prove your repayment reliability Wrapping Up!

At the end of the day, apps like Sezzle aren’t just about splitting payments; they’re about giving you breathing room. They let you say yes to what you need (and sometimes what you really want) without that immediate financial pinch. And in a world where expenses rarely wait for payday, that kind of flexibility matters.

But here’s the real takeaway: the “best” app isn’t the one with the most features—it’s the one that fits seamlessly into your spending habits without pulling you off track. Used right, these tools can be incredibly empowering. Used carelessly, they can quietly stack up into something heavier than expected.

So explore your options, pick what aligns with your lifestyle, and stay in control of your choices. Because ultimately, it’s not about finding another way to spend, it’s about finding a smarter way to manage.

We cut through the deafening digital noise to find what truly works. Every product on our list survives a relentless, hands-on analysis—no exceptions. We do the grunt work to deliver verified, trustworthy recommendations, so you can choose the right tools with absolute confidence.

- Products Reviewed - 4,000+

- No. Of Experts - 20+

- Categories - 65+

Frequently Asked Questions

Are apps like Sezzle safe to use?

There’s no one-size-fits-all answer here. Some users prefer alternatives like Klarna or Afterpay for their wider merchant networks, while others lean toward apps with fewer fees or more flexible repayment terms. The better option ultimately depends on how and where you like to shop.

Do apps like Sezzle affect your credit score?

Sezzle Anywhere gives you a virtual card that you can use almost anywhere, both online and in-store. Once approved, your purchase is split into installments, just like a regular Sezzle transaction, making it more versatile than merchant-limited options.

Are there apps like Sezzle that offer a virtual card?

Yes, several buy now, pay later apps provide virtual cards for broader usability. Options like Klarna and Zip allow you to shop across multiple retailers, giving you more flexibility compared to platform-restricted services.

How does Sezzle Anywhere work?

Most BNPL apps don’t impact your credit score for standard use, especially if payments are made on time. However, missed payments or opting for certain financing plans may be reported, so it’s always best to read the terms carefully.

What app is better than Sezzle?

Generally, yes—reputable BNPL apps use secure payment systems and encryption. That said, safety also depends on responsible usage. Keeping track of your installments and avoiding overuse is key to making the most of these tools.

We've got more answers waiting for you! If your question didn't make the list, don't hesitate to reach out.