- What is Digital Compliance?

- Why is Digital Compliance Important?

- What are the Different Types of Compliance Impacting The IT Industry?

- Types of Compliance Requirements

- Difficulties in Implementing Digital Compliance Effectively

- What are the Pitfalls of Non-Compliance?

- In-House vs. Outsourcing: What to Choose for Data Compliance?

- Understanding the Differences Between RegTech and Digital Compliance

- Looking Ahead at the Future of Digital Compliance

- Final Thoughts on Digital Compliance in IT

Share It On:

Share It On:

Consider this scenario: you are running a business where all your digital transactions, customer interactions, and data collection are constantly scrutinized. This is how the IT landscape is working today. With evolving regulations and growing cybersecurity threats, digital compliance isn’t just a legal necessity—it’s a business imperative. Top companies are failing to meet regulatory compliance standards and risking hefty fines, data breaches, and reputational damage.

But let’s try to be real- it is not easy to keep up with regulations like GDPR, ADA, WCAG, or HIPAA. There's some good news for you! Having a properly planned compliance strategy can turn your challenge into a competitive edge. Digital compliance can help businesses to stay secure, build customer trust, and avoid hefty/costly pitfalls. This ensures the safeguarding of sensitive data and ensuring seamless business operations.

But there's more to it. Dive into this guide, where we will break down what is digital compliance, why it matters, and how today's businesses can incorporate it effectively in an ever-changing digital world.

What is Digital Compliance?

Digital compliance, in simple terms, refers to ensuring that a company adheres to all legal, regulatory, and ethical requirements in its digital operations. Maintaining trust, preventing legal repercussions, and safeguarding sensitive data depend on strong digital compliance.

Businesses looking to adhere to legal requirements and safeguard confidential information must practice digital compliance. Because cyber risks are getting more complicated, companies need to make sure that their operations meet the standards of established regulations. Maintaining a trustworthy relationship with customers and regulatory agencies is just as important as protecting data from leaks, fraud, and unauthorized access. This creates a strong need of compliance for almost all digital-first businesses today.

Many industries, including banking and finance, are facing increasing pressure to comply with regulatory bodies and industry standards. By following these guidelines, operational risks are reduced, and possible cyber threats are avoided. Implementing strong security measures, guaranteeing data integrity, and upholding open procedures are all part of digital compliance rules.

Why is Digital Compliance Important?

Maintaining customer trust, preventing legal repercussions, and safeguarding sensitive data depend on how strong your digital compliance practices are. For organizational data resources to remain secure, private, and intact, digital compliance is essential. Non-compliant businesses may have severe consequences, depending on the standards in question.

Serious financial penalties that can bankrupt a company can be imposed for non-compliance with regulatory compliance criteria. A recent fine of $1.3 billion was imposed on Meta for failing to comply with GDPR while transferring users’ personal data from the EU to the US.

HIPAA infractions have cost more than $134 million since the law's creation in 2003. Businesses that violate PCI-DSS may be subject to monthly fines until the problems are fixed, and if they violate the system repeatedly, they may lose their merchant status, which would essentially force them out of business.

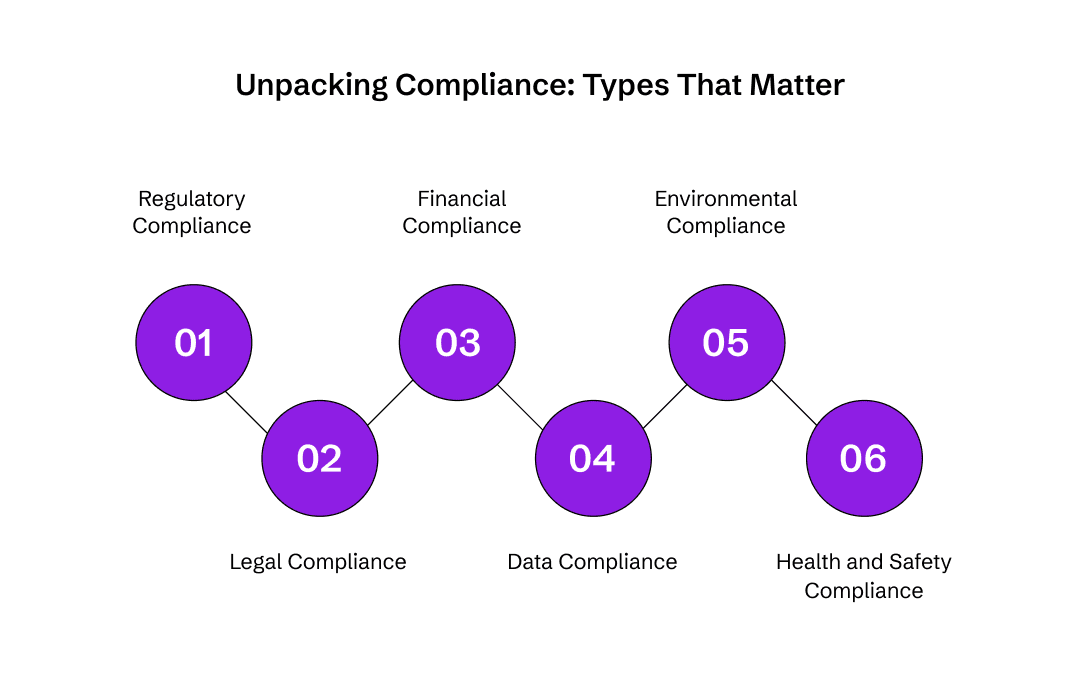

What are the Different Types of Compliance Impacting The IT Industry?

There are various types of compliance that IT companies must understand. Organizations must follow a particular set of rules or guidelines that correspond to each category. Data, financial, legal, and regulatory compliance are a few types of compliance that are frequently seen.

Regulatory Compliance

Adherence to laws, rules, and directives issued by regulatory organizations is referred to as regulatory compliance. Businesses need this kind of compliance since it guarantees that they are functioning inside the law. Popular examples include:

- General Data Protection Regulation (GDPR)

- Payment Card Industry Data Security Standard (PCI DSS)

- Health Insurance Portability and Accountability Act (HIPAA)

Legal Compliance

Legal compliance is the process of adhering to the laws and rules that legally bind a company, group, or individual. It guarantees that the activities, procedures, and conduct of an organization comply with the law. The legal compliance covers areas like:

- Contracts: Contract law, intellectual property law (copyright, patents, trademarks)

- Employment: Labor laws, anti-discrimination laws

- Taxation: Tax laws, reporting requirements

- Licensing: Business licenses, software licenses

Following the law helps businesses stay out of trouble with the law, avoid penalties, and stay out of trouble with the law.

Financial Compliance

Financial compliance is the term used to describe following the laws, rules, and guidelines pertaining to financial transactions and reporting. Compliance with laws such as the Sarbanes-Oxley Act (SOX), which requires financial reporting to be accurate, is part of this. Sustaining financial integrity and investor confidence requires financial compliance.

Data Compliance

Data compliance centers on managing data in accordance with relevant laws and guidelines, emphasizing data security, integrity, and confidentiality. This is especially critical in today's digital landscape. Examples include:

- Privacy: GDPR, CCPA (California Consumer Privacy Act), data breach notification laws

- Security: ISO 27001, NIST Cybersecurity Framework

IT Compliance Frameworks

Organizations often leverage established frameworks to manage IT compliance effectively. These frameworks provide guidance on implementing and maintaining robust compliance programs. Examples include:

- NIST Cybersecurity Framework: Offers a set of standards, guidelines, and best practices to manage cybersecurity risks.

- ISO 27002: Provides guidance on information security management systems.

- COBIT: A framework for IT governance and management best practices.

Types of Compliance Requirements

Compliance isn’t a one-size-fits-all approach—different industries face different regulations. From data security to workplace safety, businesses must navigate multiple requirements to avoid legal trouble. Below are key categories from the regulatory compliance list that companies must follow.

1. Data Protection and Privacy (GDPR, HIPAA, PCI DSS)

Protecting customer and employee data is non-negotiable. The GDPR, or General Data Protection Regulation, requires every business handling EU citizens’ data to ensure privacy and security. In the same way, HIPAA or the Health Insurance Portability and Accountability Act can enforce strict data protection in the healthcare industry.

Companies processing payment information must comply with PCI DSS to prevent fraud. Ignoring these can lead to massive fines—Amazon was hit with a €746 million GDPR fine in 2021.

2. Workplace Safety and Employee Protection (OSHA, Compliance Plans)

Every business must ensure workplace safety. The Occupational Safety and Health Administration (OSHA) enforces safety measures to prevent hazards. Additionally, businesses need a compliance plan to outline internal procedures for adhering to industry regulations. If neglected, companies risk severe penalties—construction firm Atlantic Drain faced $1.5 million in fines after a fatal trench collapse.

3. Financial and Corporate Governance (SOX, Financial Compliance)

For every business, it is crucial to ensure adherence to digital compliance and accurate financial reports. The SOX or Sarbanes-Oxley Act mandates firm corporate governance, while other compliance regulations like AML or Anti-Money Laundering laws can help to prevent fraud. Any company failing these standards can face severe consequences just like the case happened with Wirecard in 2020, where the company collapsed because of an accounting fraud.

4. Cybersecurity and IT Compliance (Cybersecurity Standards)

In an era of cyber threats, including social engineering attacks, enterprise compliance standards demand strong security measures. Cybersecurity compliance frameworks like NIST and ISO 27001 help businesses protect sensitive data. Without them, breaches can be catastrophic—Equifax paid $700 million in fines after a preventable data breach exposed 147 million records.

Understanding these compliance categories highlights why digital compliance's importance is growing. Companies that proactively integrate compliance into their operations avoid financial, legal, and reputational damage.

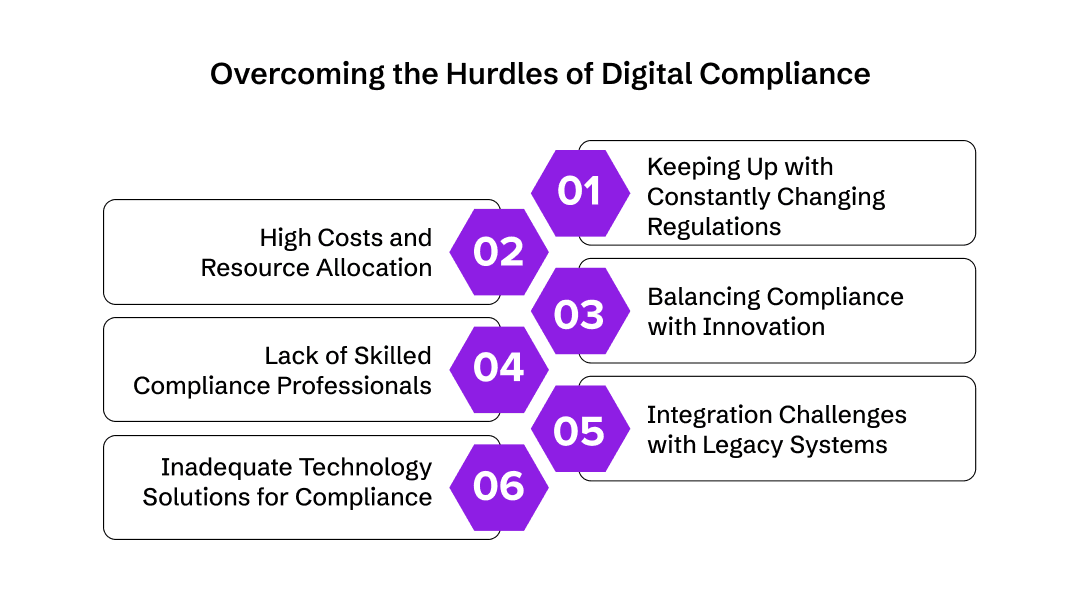

Difficulties in Implementing Digital Compliance Effectively

Are you prepared for the next wave of regulatory changes? In the IT industry, compliance is no longer optional—it's a necessity. The penalties for non-compliance are steep, and the regulatory landscape is becoming increasingly complex. This article cuts through the noise and highlights the critical challenges IT companies face in staying compliant, offering insights into how they can protect themselves and their businesses.

1. Keeping Up with Constantly Changing Regulations

One of the biggest challenges is the ever-evolving regulatory compliance list that businesses must adhere to. Laws like GDPR, CCPA, and HIPAA update frequently, and failing to adapt can lead to heavy fines.

In 2023, Meta faced a record-breaking €1.2 billion fine for non-compliance with GDPR. Businesses can struggle to keep pace with these changes without a dedicated compliance team or automated solutions.

2. High Costs and Resource Allocation

Ensuring digital accessibility compliance isn’t just about policies—it requires technology, training, and audits. Small and mid-sized companies often lack the resources to maintain compliance without sacrificing growth.

For example, a financial institution implementing SOC 2 compliance must invest in cybersecurity infrastructure, employee training, and regular audits, which can cost thousands annually. If neglected, a single data breach can be even more expensive.

3. Balancing Compliance with Innovation

The need of compliance is clear, but it often conflicts with business agility. Tech companies racing to launch new products may see compliance as a roadblock. If security reviews delay software releases, competitors might gain an edge. However, skipping compliance steps can lead to legal trouble—think of Uber’s past struggles with data protection violations. Striking a balance between compliance and innovation is a challenge every IT business faces.

Without a proactive approach, regulatory compliance becomes a liability instead of an asset. Companies that invest in structured policies, automation, and expert guidance can avoid financial penalties and gain a competitive advantage in today’s digital landscape.

What are the Pitfalls of Non-Compliance?

Non-compliance isn’t just a bureaucratic headache—it’s a business risk that can cost millions, damage reputations, and even lead to legal consequences. Many companies assume that cutting corners in compliance saves time, but in reality, it exposes them to penalties, security breaches, and loss of customer trust. Understanding the risks makes compliance initiatives a priority, not an afterthought.

1. Financial Penalties and Legal Action

Regulators don’t take violations lightly. Companies that fail to meet regulatory compliance standards face hefty fines. For instance, British Airways was fined $230 million under GDPR for a data breach.

Similarly, Wells Fargo paid $3 billion for fraudulent banking practices. These penalties highlight the cost of overlooking enterprise compliance standards—what seems like a minor oversight can quickly escalate into a major financial burden.

2. Reputation Damage and Customer Trust Loss

Trust takes years to build but only seconds to lose. A single compliance misstep can tarnish a brand’s reputation. When Facebook (now Meta) mishandled user data in the Cambridge Analytica scandal, it not only faced a $5 billion fine but also lost public trust. Companies investing in compliance initiatives avoid such crises and ensure customers feel secure when sharing their information.

3. Operational Disruptions and Business Risks

Regulatory investigations and legal battles drain company resources. Non-compliance often leads to operational slowdowns, revoked business licenses, or even shutdowns. When Volkswagen’s emissions scandal came to light, it faced billions in fines and a halt in sales for non-compliant vehicles. This shows the digital compliance importance that goes beyond avoiding fines—it safeguards business continuity and long-term growth.

Ignoring compliance is a gamble no company should take. Investing in strong enterprise compliance standards ensures businesses operate smoothly, avoid unnecessary risks, and maintain a competitive edge.

In-House vs. Outsourcing: What to Choose for Data Compliance?

When it comes to ensuring regulatory compliance standards, businesses often debate between managing everything in-house or outsourcing to experts. While both options have their merits, outsourcing offers significant advantages, especially for companies that lack the resources, expertise, or time to handle complex types of compliance requirements on their own. Let’s break down why outsourcing is the smarter choice for achieving airtight compliance.

1. Expertise and Specialized Knowledge

In-House: Building a dedicated compliance team requires hiring skilled professionals who understand data protection laws like GDPR, CCPA, and HIPAA. However, regulations are constantly evolving, making it difficult for an internal team to stay up to date.

Outsourcing: Compliance service providers specialize in handling types of digital compliance, ensuring businesses remain compliant without having to track every regulatory change. They work with multiple clients across industries, gaining exposure to different compliance challenges and solutions.

Example: A healthcare startup struggling with HIPAA compliance might find it easier to work with an external firm specializing in healthcare data security rather than training an internal team from scratch.

2. Cost-Effectiveness and Resource Allocation

| Factor | In-House | Outsourcing |

|---|---|---|

| Hiring Costs | High – Requires full-time compliance officers and legal experts | Low – Pay only for the service you need |

| Training & Updates | Expensive – Ongoing training is needed to keep up with changing regulatory compliance standards | Cost-effective – Experts stay updated without additional training expenses |

| Technology Investment | Requires in-house software and security infrastructure | Service providers use advanced compliance tools at no extra cost |

For many companies, the need of compliance is crucial, but maintaining an in-house team can drain resources. Outsourcing allows businesses to focus on their core operations while compliance is managed efficiently by professionals.

3. Scalability and Flexibility

In-House: If a company expands into new markets or industries, its compliance team must adapt to new types of compliance requirements—which can mean hiring more experts, revising policies, and investing in new compliance tools.

Outsourcing: Third-party compliance firms already operate at scale. Whether a business expands domestically or internationally, it provides tailored solutions that align with regional regulatory compliance standards without additional overhead.

Example: A fintech startup expanding from the U.S. to Europe would need to comply with both CCPA and GDPR. Instead of building separate compliance teams for each region, outsourcing provides an instant solution with global expertise.

4. Risk Mitigation and Legal Protection

In-House: If internal teams miss an update in compliance laws, the business is solely responsible for penalties. The risk of non-compliance remains high, especially in industries with stringent regulations.

Outsourcing: Compliance service providers offer risk assessments, audits, and legal support, significantly reducing exposure to fines and lawsuits. Many firms even provide liability protection, sharing responsibility if something goes wrong.

Example: When Equifax faced a $700 million penalty for a data breach, it highlighted the dangers of weak compliance infrastructure. Outsourced compliance firms proactively monitor risks, preventing such costly failures.

The Result: Outsourcing Wins for Most Businesses

For companies that prioritize efficiency, cost savings, and risk reduction, outsourcing compliance is the smarter choice. It provides expert support, scales with business needs, and ensures compliance is handled by professionals who specialize in staying ahead of regulations.

If you’re looking for a reliable partner to manage the types of digital compliance, explore our directory of software development companies and mobile app development companies. These firms specialize in building secure, compliant systems, ensuring your business meets all regulatory compliance standards without the hassle of an in-house team.

ALSO READ: How to outsource software development

Understanding the Differences Between RegTech and Digital Compliance

The phrase "Digital Compliance" has been gaining traction alongside the term "RegTech." However, what distinguishes these two from one another?

First, let's talk about RegTech. Most business users understand that RegTech refers to ways that new technologies can be applied to regulatory processes—modernizing or changing them—given the term's widespread usage and obvious "buzzword" status. Generally speaking, the phrase "RegTech" refers to the application of cutting-edge technological solutions to handle a single regulatory difficulty, such as those that use sophisticated analytics to identify possible money laundering situations. The word "RegTech" comes from the more general term "FinTech," which describes how new technology might be used to improve a variety of conventional financial services procedures.

The phrase "digital compliance" has just lately gained popularity. In our opinion, the phrase "digital compliance" refers to a much larger idea that examines the entire compliance process rather than just a single remedy to a particular regulatory issue. Digital Compliance is more than just launching a RegTech solution; it also includes changing how teams use these products and how to optimize the process to maximize their benefits.

These high-level ideas are simple to understand, but it's unclear how much more in-depth knowledge of the technology should be expected of compliance and risk experts. An unofficial survey of Synechron customers revealed a wide variety of opinions regarding RegTech. On the one hand, people are completely doubtful, wondering if any of these new data analytics and technology tools are much better than those that are already on the market.

After all, in order to handle regulatory compliance, financial institutions already employ advanced technology in their operations. On the other end of the spectrum, people go to considerable lengths to be receptive to the advantages of new technology, perhaps without fully understanding the concrete advantages these instruments might offer.

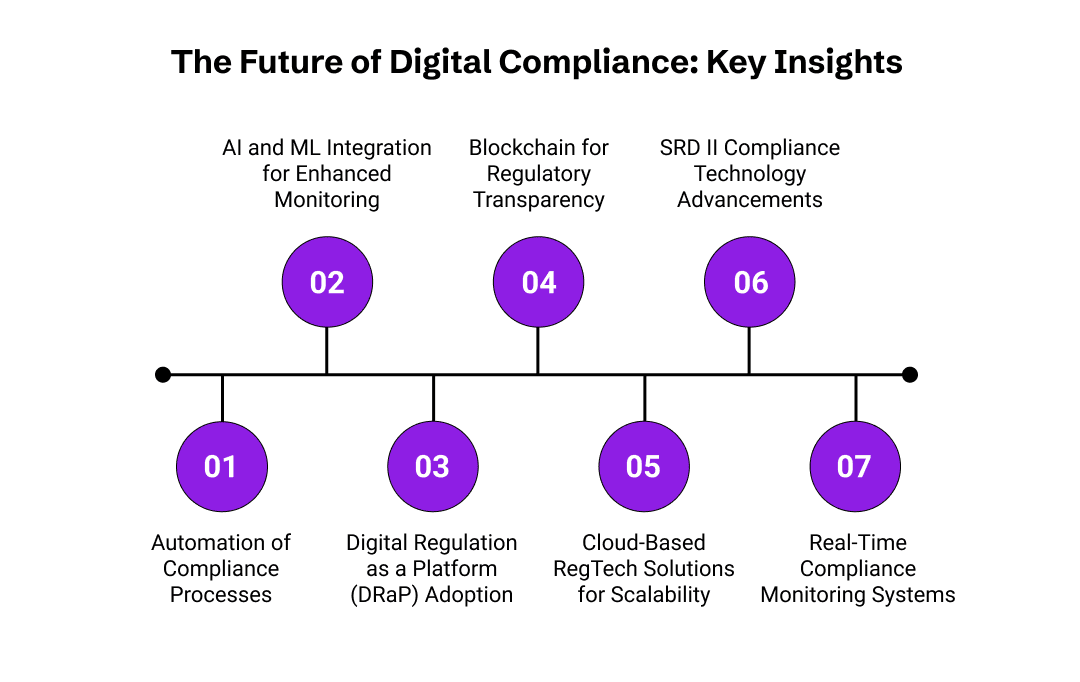

Looking Ahead at the Future of Digital Compliance

By far, we have found in-depth answers to ‘what is digital compliance’ and understood that it has several concepts around it. But what about the future?

As businesses continue to embrace digital transformation, compliance is evolving beyond manual audits and paperwork. The future lies in automation, AI-driven monitoring, and integrated platforms that streamline compliance management while reducing risks and costs.

Digital Regulation as a Platform (DRaP)

One promising innovation is Digital Regulation as a Platform (DRaP), a concept that digitizes regulatory processes using rule-based algorithms. Originating from Australia's Regulations as a Platform (RaaP) model, DRaP enables free and open access to legislation via public APIs. By incorporating Rules as Code (RaC) and Compliance Management Systems (CMS), DRaP ensures automated compliance, real-time monitoring, and seamless enforcement.

As industries move forward, businesses must prepare for stricter, technology-driven regulatory landscapes. Adapting to these changes early on will be crucial in maintaining compliance, avoiding penalties, and staying ahead in an increasingly digital world.

Artificial Intelligence (AI) and Machine Learning (ML) in Compliance

Every facet of the company is changing due to AI and ML, and regulatory compliance is no exception. Automating intricate compliance procedures like fraud detection, transaction monitoring, and customer due diligence is becoming more and more important thanks to these technologies.

According to a new IndustryARC analysis, the RegTech artificial intelligence market is expected to develop at a compound annual growth rate (CAGR) of 36.1% from 2021 to 2026, reaching $3.3 billion. The reason for this growth is that AI systems are able to analyze enormous volumes of data at previously unheard-of rates, finding patterns that human analysts might overlook. This aids in the fight against financial crimes.

The way compliance departments function is being revolutionized by the capacity to process large datasets rapidly and accurately. By learning from past data and anticipating possible compliance violations, AI also improves the accuracy of compliance assessments. As machine learning models advance, the number of false positives in compliance alerts decreases. AI-powered systems, for example, can assist financial institutions in automating the reporting process to regulatory bodies, flagging suspicious activity, and monitoring consumer transactions in real time.

Blockchain to Enhance Regulatory Transparency and Safety

Another significant development that is influencing the use and direction of RegTech is blockchain technology. The decentralized, unchangeable ledger of blockchain technology is especially useful for enhancing financial transaction security and transparency, both of which are essential for regulatory compliance. Blockchain can assist organizations in maintaining the integrity of their compliance data by making sure records are impenetrable, lowering the possibility of errors and fraud.

Blockchain has gained widespread recognition in recent years as a universal answer to a number of problems. However, some have begun to doubt the use of blockchain technology due to the extended decline in the cryptocurrency market and the heightened regulatory crackdowns on initial coin offerings.

However, there have been hopeful advancements in the usage of blockchain for RegTech solutions, as it is being applied more and more to improve KYC process efficiency and minimize effort duplication among financial institutions.

Blockchain makes it possible for institutions to safely exchange client data, doing away with the need for numerous verification processes while maintaining regulatory compliance. This lowers compliance expenses while also expediting the onboarding process.

Additionally, the auditable record of transactions that blockchain offers streamlines the reporting process and makes it simpler for authorities to confirm compliance. The growing significance of blockchain technology in the RegTech industry is further highlighted by the World Economic Forum's prediction that 10% of the world's GDP will be kept on blockchain platforms by 2027.

Cloud-based RegTech Solutions for Scalability

Cloud-based RegTech solutions are quickly emerging as the preferred choice for scalability and flexibility as financial institutions continue to embrace digital transformation.

Without requiring significant infrastructure investments, cloud computing allows organizations to swiftly and effectively implement regulatory compliance solutions. The unmatched scalability that cloud-based RegTech solutions currently provide makes it simpler for financial institutions of all sizes to adjust to changing regulatory requirements.

Additionally, cloud solutions make it easier for departments and locations to collaborate, which makes it possible for compliance data to be shared easily within an organization. This is especially crucial in today's globalized financial environment, where laws differ from one country to another.

These technologies enable businesses to retain global operational efficiency while adhering to local regulations. The growing need for adaptable and scalable compliance solutions is expected to fuel the growth of the global cloud-based RegTech market, which is expected to reach $16.4 billion by 2026 from $6.3 billion in 2021, according to research by Markets and Markets.

SRD II Compliance Technology

The legal environment in Europe has been profoundly altered by the Shareholder Rights Directive II (SRD II), and RegTech companies are creating solutions to assist businesses in meeting its intricate requirements.

SRD II seeks to enhance corporate governance and shareholder involvement in EU-listed businesses. By automating shareholder identification and authentication, enabling secure communication between businesses and shareholders, and expediting the proxy voting process, RegTech solutions are helping financial institutions adhere to SRD II.

For financial institutions aiming to adhere to the Shareholder Rights Directive II (SRD II) in 2024, decoding SRD corporate action alerts has become a crucial task. These notifications are crucial for preserving openness between businesses and shareholders because they convey important events like mergers, dividend payments, and proxy voting.

However, deciphering and reacting to these notifications can be difficult and time-consuming. In order to ensure correct and timely responses and lower the risk of non-compliance with SRD II laws, digital solutions are automating the decoding of disclosure mailings.

In addition, these solutions guarantee total transparency for all parties involved, which is crucial for preserving the integrity of shareholder participation. As global shareholder laws and SRD II continue to change, we anticipate more RegTech ideas to help with compliance issues.

Final Thoughts on Digital Compliance in IT

Digital compliance is no longer just a legal requirement—it’s a business necessity. With evolving regulatory compliance standards and increasing cybersecurity threats, IT organizations must adopt proactive strategies to ensure security, data integrity, and operational trust. Companies that treat digital transformation in risk and compliance as an ongoing initiative rather than a one-time obligation are better positioned to navigate the complexities of today’s digital landscape.

The future of compliance lies in automation, AI-driven monitoring, and integrated frameworks like Digital Regulation as a Platform (DRaP). By embracing these advancements, businesses can streamline their compliance efforts while reducing costs and risks. Whether it’s enterprise compliance standards, types of compliance requirements, or the need of compliance in IT, organizations must stay ahead by continuously evolving their strategies.

Ultimately, digital compliance is about more than just following rules—it’s about building trust, securing data, and ensuring long-term success in an increasingly regulated and digital-first world.

Frequently Asked Questions

What is the need of compliance in the digital landscape?

What are the different types of digital compliance?

Why is digital accessibility compliance important?

What are common types of compliance requirements for businesses?

What is regulatory compliance?

Where can I find a regulatory compliance list for my industry?

What are enterprise compliance standards?

What is the importance of digital compliance?

What are the pitfalls of non-compliance?

How can compliance initiatives benefit my organization?

Uncover executable insights, extensive research, and expert opinions in one place.