Blockchain is a technology that mainstream businesses are adopting rapidly, compelling the remnant stakeholders to explore the question, “What is blockchain technology?.”

Blockchain is a technology that mainstream businesses are adopting rapidly, compelling the remnant stakeholders to explore the question, “What is blockchain technology?.”Thinking about implementing blockchain technology for your business or enterprise?

Utilizing blockchain technology can unlock unhindered and enhanced data-sharing capabilities, data immutability, and transparency for your business. However, implementation of the technology demands a clear understanding of the question, “What is Blockchain Technology?”

Understanding this requirement, we have developed this basic guide to familiarize you with the concept of blockchain in detail. Plus, there are some bonuses integrated into the editorial to ease up your blockchain experience. So, explore ahead as we take you through the terrain of understanding blockchain technology in its essence.

What Is Blockchain Technology?

Blockchain, as a technology, has created waves in the IT industry in recent years. This is the reason everyone is looking to grab a piece of the pie. However, to truly understand it, we need to start with the meaning of blockchain.

Establishing “blockchain meaning,” well, it is a system that records transactions, especially those that belong to cryptocurrency. These records are maintained across computers and linked through peer-to-peer networks.

However, if we have to simplify the explanation, here is the analogy. Think of blockchain as a document, but it is not a single copy. Instead, it is distributed to everyone. This means that everyone has the recorded data collected during transactions. Now, to make any bit of change to the recorded data, the permission of relevant parties will be required, making it almost impenetrable to hacking or alteration.

Key Features of Blockchain Technology - Exploring Its Capabilities

Blockchain as a technology offers multiple features that play a key role in its adoption, especially when it comes to securing records for businesses. Stating this, here are the key features that fuel the need for blockchain in business:

- Decentralization: Blockchain essentially works on the concept of decentralization. This means that there is no single person that can control or operate blockchain ledgers.

- Immutability: The data points collected within the blockchain ledger can’t be altered or deleted without permission from relevant parties.

- Transparency: Ledgers of blockchain are available publicly for anyone to view, in general.

- Security: Considering its decentralized nature, blockchain technology has a keen focus on utilizing powerful cryptography techniques like hashing and encryption, with many experts discussing how blockchain impacting mobile app security is becoming increasingly relevant.

- Efficiency: To its users, blockchain delivers faster transactions and reduced costs as there are no intermediaries.

History of Blockchain - Key Events

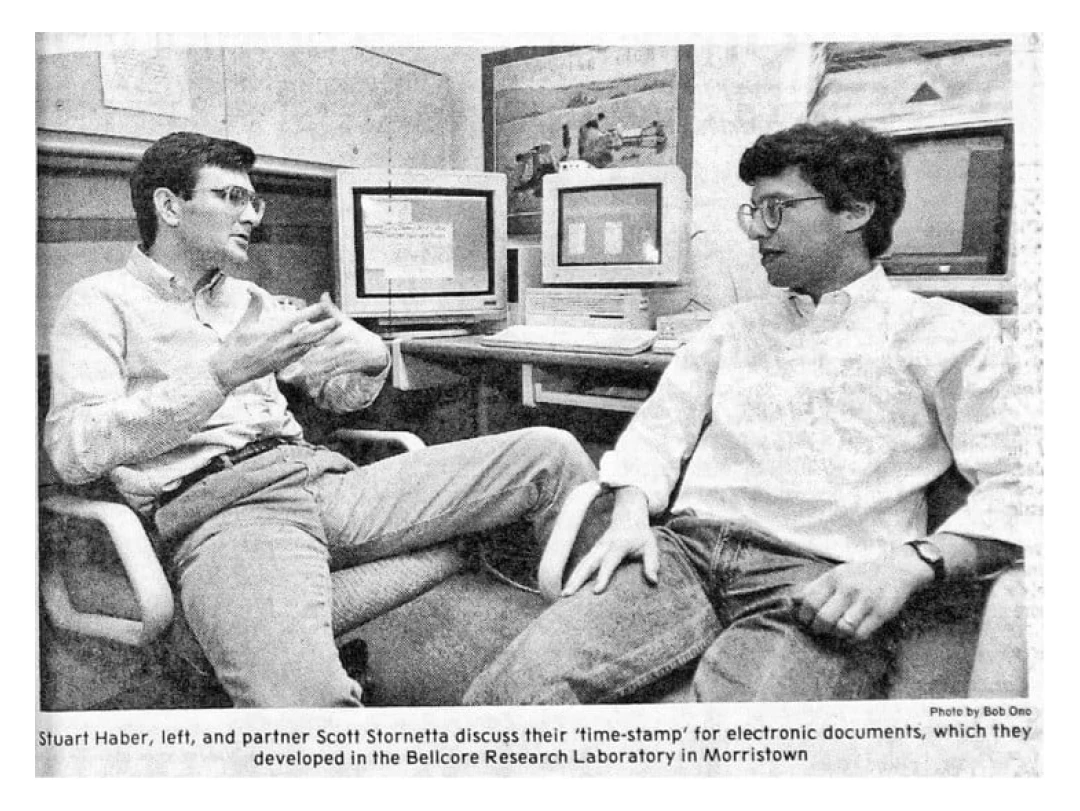

A lot of people believe that blockchain is a nascent phenomenon. However, the concept was first introduced in 1991. Stuart Haber and W. Scott Stonetta published their paper on blocks of cryptographically secured chains.

Everything in this domain was completely silent until Satoshi Nakamoto, in 2008, published his white paper introducing Bitcoin. To reignite the old flame, the Bitcoin paper was based on blockchain technology.

Bitcoin became the birth of the first blockchain network, and then later on, cryptocurrencies like Ethereum and many others in the line emerged. Each of these events became the reason behind the boom of blockchain. And, contributions like the “Hyperledger Project” by the Linux Foundation, Initial Coin Offerings, etc., started to happen. Each of these events led blockchain to its current maturity, inspiring leaders to make the most of it.

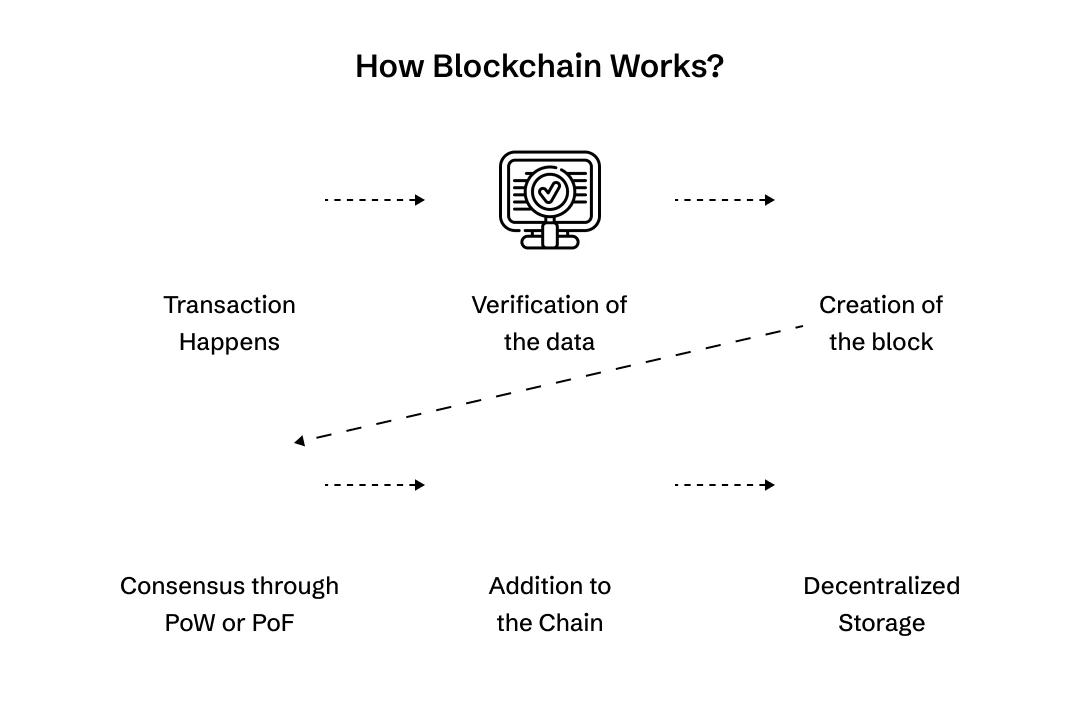

How Does Blockchain Work?

“How does blockchain work?” is a prominent question amongst stakeholders or the ones willing to adopt it. The working of blockchain involves multiple complex layers. However, to give you a gist of the working process, here are the steps taken by a blockchain system for a valid transaction.

- Transaction Happens: Imagine someone has initiated a transaction on the blockchain ledger. For instance, sending money, recording a contract, or storing data.

- Verification: Now, the transaction is sent to a network of computers or nodes for further verification. If the computer finds the transaction valid, the process jumps to the next step. Otherwise, it gets nullified.

- Block Creation: Once the verification process is over, the transaction is grouped with others in a block that carries other transaction data. This block will contain the list of transactions, timestamps, and a reference to the previous block.

- Consensus: Now, a process called Proof of Work or Proof of Stake is initiated to reach the agreement to add the block.

- Addition to the Chain: The block that is verified is added to the blockchain making it a permanent and tamper-proof part.

- Decentralized Storage: At this final stage, multiple copies of the blockchain with updated data are stored across nodes in the network, making sure that everyone has the same record.

Types of Blockchain Technologies

Blockchain is a technology that offers varied levels of accessibility and transparency depending upon the type being used. So, to help you understand the varied properties, here are the different types of blockchain available:

Public Blockchain

A public blockchain is an open distributed ledger technology that allows its participants to access, view, and add to the network without any explicit permission from any central power.

Real-Life Examples of Public Blockchain:

- Bitcoin

- Ethereum

- IBM Food Trust

- Civic

- Aave

Private Blockchain

A private blockchain involves a distributed ledger technology shared amongst a group of participants, a single organization, or a group of organizations. Not anyone can join a private blockchain network, and if someone wants to do it, they require permission from the authorities.

Real-Life Examples of Private Blockchain:

- Hyperledger Fabric

- R3 Corda

- Medibloc

- Vakt

- Dubai Blockchain Strategy

Hybrid Blockchain

A hybrid blockchain combines the power of both public and private blockchains. It contains a hybrid database that comprises both public and private entries. When it comes to access, the public entries are accessed, viewed, or updated like a public blockchain, and in the case of private entries, the user requires explicit permission.

Real-Life Examples of Hybrid Blockchain:

- Walmart Food Trust

- Maersk TradeLens

- Medibloc

- Ripple

- Polygon

Consortium Blockchain

Consortium blockchain, as the name suggests, isn’t managed by any single entity. Instead, it is managed through each organization within the consortium. This type of blockchain is used where a balance between decentralization and control is required. Overall, it is an excellent technology for several use cases where a group of companies want to collaborate and keep the rights of the data within the consortium.

Real-Life Examples of Consortium Blockchain:

- VeChain

- B3i (Blockchain Insurance Industry Initiatives)

- Trade Lens

- Enterprise Ethereum Alliance (EEA)

- Energy Web Chain

Comparing the 4 Types of Blockchain - Summarizing the Differences!

Defining and comparing are two different things. This section is the later part giving you a side-by-side comparison to clearly outline the differences between types of blockchain.

| Feature | Public Blockchain | Private Blockchain | Consortium Blockchain | Hybrid Blockchain |

|---|---|---|---|---|

| Accessibility | Open to everyone | Requires permission | Access is restricted to members of the consortium | Combination of open and restricted access |

| Control | No single entity controls the network | Controlled by a single entity or organization | Decentralized for the members of the consortium | Varies depending on the implementation |

| Transparency | Transactions are publicly visible | Only authorized users can view data | Data visibility controlled by the consortium | Combines elements of public and private transparency |

| Privacy | Low | High | Moderate | Varies based implementation |

| Governance | Decentralized | Centralized | Shared governance between associated organizations | Combination of decentralized and centralized governance |

| Performance | It can be slower due to network congestion and validation requirements | Generally faster due to fewer participants and optimized consensus mechanisms | Faster than public blockchains but slower than fully centralized private blockchains | Performance varies based on the balance between public and private components |

| Use Cases | Cryptocurrencies (Bitcoin, Ethereum), decentralized applications (dApps), NFTs | Supply chain management, financial services, healthcare, internal enterprise applications | Supply chain management, financial services, healthcare, cross-industry collaborations | Supply chain management, healthcare, cross-border payments, DeFi |

Benefits of the Blockchain - Peeling Off the Reason Behind Its Adoption!

At least from a business point of view, blockchain has several benefits. Extrapolating on that, we have created a list of the most important benefits reaped through blockchain.

- Traceability: High traceability through audit trails.

- Transparency: Immutable ledgers that are only accessible to the participants.

- Reduced Cost: Eliminates intermediaries and reduces manual tasks, reducing associated operational costs.

- Efficiency: Enables process automation, faster transactions, and simplified reconciliation.

- Security: Encrypts transactions, requires consensus for verification, and stores data across a decentralized network.

- Smart Contracts: Enables self-executing and self-verifying contracts that cannot be altered.

- Tokenization: Can represent assets like real estate, equity, or bonds as digital.

- Improved Accuracy: Removes manual human intervention, minimizing errors during verification and reconciliation.

- Decentralization: No central point leading to enhanced resilience and reduction in tampering risks.

- Real-Time Operations: Allows transactions 24/7 without any constraints.

- Data Privacy: Restricted access by using private blockchains protecting sensitive data.

- Fraud Prevention: Protection against any sort of data manipulations and identity theft securing digital identities.

- Accountability: Enhanced auditability, reduced fraud, and consistent transaction accuracy.

- Compliance: Delivers simplified auditing and regulatory adherence with transparency in records.

- Digital Currencies: Facilitates the usage of secure and efficient transactions through cryptocurrencies or tokenized money.

- Auditing: End-to-end tracking and verification of the supply chain processes and other related transactions.

- Global Adoption: Supported across industries for diverse applications and investor backing all around the world.

- Decentralized Network: Sustains data integrity and availability even if all the nodes fail.

- Programmability: Allows users to create custom logic and automation using the programmable features.

- Innovation Potential: Has the potential to solve complex problems and reshape inefficient practices.

- Improved Data Quality: Allow the storage and regulation of tamper-proof data.

Limitations of Blockchain Tech

Now, since we have already talked about the benefits of the blockchain, it's time to assess its limitations. So, here we go:

- High-volume transactions can be a hassle with many blockchains.

- Mechanisms around the Proof-of-Work concept used by Bitcoin require a lot of computation energy.

- Regulations around blockchain are still evolving in many jurisdictions.

- Lack of privacy is an ongoing issue in public blockchains.

- Immutability can make it difficult to rectify incorrect data.

- Complex to understand and implement.

- The different types of blockchains can have issues communicating with each other.

Blockchain Use Cases

If we start to discuss the sheer number of blockchain use cases, then it would be a separate editorial. However, here are some of the most implemented use cases of blockchain commonly in the real world.

1. Finance

The application of blockchain in Fintech is majorly around leveraging the technology’s security and transparency of transactional records. Blockchain in Fintech has tonnes of use cases where the tech is rampantly used. For instance:

- Cryptocurrency: Digital currencies like Bitcoin, Ethereum, and other cryptos use blockchain to secure and decentralize transactions.

- Decentralized Finance (DeFi): These are blockchain-based platforms that are used for lending, borrowing, trading, and other financial transactions.

- Cross-border Payments: It facilitates faster and more cost-effective transfer of money internationally.

- Securities Trading: It can be used to streamline the issuance and trading of securities. For instance, stocks and bonds.

2. Supply Chain Management

Pharmaceuticals, food and agriculture, automotive, logistics, etc., are some industries that make use of blockchain for supply chain management. And with good reason, as each industry gets relevant help with the application of blockchain in their business, such as:

- Tracking and Traceability: The application of blockchain can enhance transparency and accountability of the supply chains by tracking the origin and movement of the goods.

- Reducing Counterfeit Goods: Blockchain can help verify the authenticity of any product to prevent the distribution of counterfeit items.

- Improving Food Safety: Blockchain can enable the tracking of food products catering to the complete supply chain from farm to table, reducing the risk of contamination.

3. Healthcare

In healthcare, the importance of fast and secure sharing of data is enormous. This is the reason blockchain in healthcare plays an important role in the aforementioned. However, there is more to the picture.

- Pharmaceutical Supply Chain Management: The application of blockchain increases the traceability of the movement of pharmaceutical supplies. Its secure nature ensures authenticity while preventing counterfeits.

- Decentralized Electronic Health Records (EHRs): EHRs are sensitive patient data, and even if a firm doesn’t want to secure them, HIPAA compels them to do so. With blockchain, due to its decentralized nature, the process of accessing, viewing, and altering the data becomes secure if a private or consortium blockchain is used.

- Healthcare Payments and Insurance: Claims processing is an essential part of the insurance process. Using blockchain, not only can this process be eased, but the cost surrounding it can also be minimized. Plus, due to blockchain’s immutable nature, detecting fraud also becomes very easy.

4. Government

Do you know about the Dubai Blockchain Strategy? Well, the government of Dubai wants to make itself the global leader in blockchain technology. And, for that, they are taking several initiatives like digitization of government services, blockchain-based economy, establishment of regulatory framework, etc.

Likewise, governments all around the world can think about blockchain, maybe not to this effect, but the technology can solve multiple issues.

- Secure Voting Systems: Fraud in elections often makes the headlines in the news. But through blockchain, the process can be made transparent with reduced risk maintaining the integrity and accuracy of vote tallies.

- Land Registries: Land registries are another important use case that requires efficient and secure ownership records. Blockchain can make that happen, reduce land frauds and disputes, streamline property transactions, and whatnot.

- Identity Management: Securing identities is another use case that requires security and a tamper-proof nature in many nations. Extrapolating on that, blockchain can make the digital identities of citizens secure and tamper-proof, + the speed of the service will also increase.

5. Real Estate

Real Estate is another industry that heavily benefits by investing and implementing blockchain. Some ways it can help are:

- Smart Contracts: Transactions like sales, rentals, etc., can be automated using blockchain.

- Tokenization of Real Estate: Blockchain enables fractional ownership of real estate assets.

Besides the blockchain use cases mentioned above for different industries, there are many others, like the Internet of Things (IoT), Decentralized Autonomous Organizations (DAOs), Legal & Judicial, etc., that can make use of blockchain.

Emerging Trends in Blockchain

Blockchain, as a technology, has evolved since its inception and has gone through a variety of market dynamics. Still, Richard Teng (CEO of Binance) says, “If you look at past cycles, this year will be a year that we see a new all-time high for the crypto industry.”

He attributes this analysis to the positive sentiment he saw amongst politicians and corporations, attributing to its growth. Keeping this in mind, there will be tonnes of blockchain trends that the industry is likely to witness in the coming years.

So, extending his analogy, here are some of the emerging trends of blockchain that may either become prominent or see the light of the market.

- The industry focus of blockchain is on improving communication through relay chains and hubs, with the aim of creating a more connected, scalable, and decentralized ecosystem.

- User-controlled assets and decentralized governance will come into play as advanced financial instruments like DEXs, algorithmic stablecoins, etc., become advanced.

- Greener and more sustainable blockchain practices with more usage of energy-efficient consensus mechanisms (PoS and DPoS).

- NFTs will see broader applications beyond art, collectibles, etc., due to the core interest of the industry in the tokenization of real-world assets, gaming integration, etc.

- Compliances will improve in sectors like finance and healthcare with cryptographic implementations like zk-SNARKS, zero-knowledge proofs, etc.

- The voting process might become more transparent via smart contracts creating an open and democratic organizational structures.

- The adoption of blockchain will be simplified through cloud-based platforms and emerging blockchain smartphones technology, making solutions more cost-efficient and adaptable.

MobileAppDaily-as-a-Service: How it Can Help?

MobileAppDaily is a consortium of different resources associated with IT, helping our audience gain knowledge and gauge success in the highly competitive landscape. To ensure this, through hard work, we have developed tonnes of well-researched resources in different categories. For instance, Editorials, Top Products Reports, Exclusive Interviews, Web Stories, and whatnot.

However, our resources that can immensely help are our reports on top blockchain development companies. In fact, we have dug deeper and prepared reports on requirements like Top Blockchain Development Companies in India, Best NFT Development Marketplaces, Best dAPP Development Companies, etc. With each of these resources, we aim to catapult our audience toward business success and create a symbiotic relationship that aids you with knowledge and MobileAppDaily with more prominence in the market.

Concluding It!

The application of blockchain technology is across borders and industries. From finance to healthcare, every industry has some key players that are using blockchain to transform their offerings and making them more secure and transparent, clearly showing how blockchain changing mobile app industry and digital ecosystems overall. And, considering the intent of the editorial, we believe that you needed acute knowledge around the tech to fully leverage it.

In this process, getting the answer to “What is Blockchain Technology?” can help you fully harness its prowess. With this editorial, our aim has also been to provide you with a basic understanding of blockchain technology, covering each of its nooks and corners and helping you effectively implement it. Saying this, if you liked this editorial, you can also check our blog section for more exciting resources.

Frequently Asked Questions

What is blockchain for beginners?

Understanding the blockchain isn’t tricky.

Simply imagine a digital ledger that is distributed in the network. Each of the associated individuals has a copy, and if there is any alteration or update in the data, this information will also reflect in each copy of the ledger.

However, it is important to note that the accessibility feature of blockchain changes with its types, such as public, private, hybrid, and consortium. For more clarity, check out these properties:

- Decentralized, i.e., no single entity controls it.

- Immutable so that no data can be altered or deleted without relevant permissions.

- Use of cryptography to secure transactions and data.

- Transparency, as the ease of viewing the blockchain records, changes with the property of the blockchain implemented.

How does blockchain work?

Imagine blockchain as a chain of blocks that contains information. So, once a block is added to the network, it becomes permanently linked to the previous block. These blocks are like a shared notebook that everyone can see. However, no one can erase or change them without relevant permissions.

What are the types of blockchains?

Categorically, there can be many types, but conceptually, there are primarily four types of blockchains:

- Public Blockchains: Anyone can join and no single authority control the network.

- Private Blockchains: Provides access and data manipulation control to authorized participants.

- Consortium Blockchains: Access granted to a group of selected organizations.

- Hybrid Blockchains: Offers features of both public and private blockchains.

Are there any blockchain examples in business?

In terms of business examples, there are many in the context of business. Stating them, here are those examples:

- Supply Chain Management: Walmart, Unilever, and Maersk.

- Financial Services: JPMorgan Chase, Ripple, and HSBC.

- Healthcare: IBM Food Trust, MediLedger, and Microsoft.

- Real Estate: Propy, Land Registry (in some countries), and Smart Contracts in general.

What are the benefits of blockchain in business?

There are many benefits of blockchain in business if adopted. They are:

- Reduces the cost of intermediaries.

- Permanent records that are accessible by all enhance transparency.

- Decentralized system and immutable records.

- Capability to track products and services.

- Can help in creating digital product passports.

- It can be used to create self-executing contracts.

Can blockchain be applied to business process management challenges and opportunities?

Yes, blockchain can be applied to many challenges and opportunities in business process management (BPM) like:

- It can help promote trust and transparency because of its decentralized and transparent nature.

- Facilitates secure data sharing across different data silos within organizations and departments.

- Can implement self-executing smart contracts, streamlining the process.

- Its tamper-proof nature can prevent fraud and counterfeiting challenges.

- Blockchain can enable new business models like decentralized autonomous organizations (DAOs) and tokenized assets.

- It can help adapt to new business opportunities and changing market dynamics and demand.

What are some blockchain applications for business?

Blockchain in business has tonnes of applications, such as:

- Increasing transparency and traceability for the supply chain.

- Secured financial transactions across borders for financial services.

- Data security for patient data and streamlining of medical records.

- Simplification and securing transactions related to real-estate paperwork.

- Reducing fraud and identity theft in identity management.

- Enhancing security and transparency in voting systems.

What are some applications of blockchain in Fintech?

Here are some applications of blockchain associated with Fintech:

- Cross-border payments

- Peer-to-peer payments

- Micropayments

- Lending and borrowing

- Trading and investing

- Asset tokenization

- Trade finance

- Supply chain visibility

- Auditing and Reporting

Besides these, there are tonnes of other applications too.

What are some advantages of blockchain in the supply chain?

Several advantages of using blockchain in the supply chain are:

- Better traceability and transparency.

- Increased efficiency and reduced cost of operations

- Enhanced security and trust with data.

- Improved sustainability through the promotion of ethical sourcing and reduced waste.

How ideal is blockchain for supply chain transparency?

Blockchain technology has been developed keeping transparency in mind. By implementing blockchain in the supply chain, you get:

- Unaltered record

- Real-time tracking

- Enhanced traceability

- Increased trust and collaboration

- Reduced fraud and errors

What is a crypto blockchain?

Crypto blockchain is the technology that fuels cryptocurrencies like Bitcoin and Ethereum. It is decentralized, has a distributed ledger, and is connected through a peer-to-peer network.

What is decentralized finance?

Decentralized Finance, or DeFi, is an evolving financial system that is built on blockchain technology. With DeFi, it is possible to remove intermediaries like banks and brokers, offering a much more open, accessible, and transparent alternative.

How are blockchain and cryptocurrency related?

Cryptocurrency is the digital or virtual currency which uses cryptography for its security. On the other hand, Blockchain is a decentralized and distributed ledger that records and verifies transactions related to cryptocurrency.

Here’s an analogy to understand the relationship between blockchain and cryptocurrency. If you are the owner of a couple of bitcoins, then the blockchain is the spreadsheet that keeps a record of it and verifies the data that everyone can see in the network.

Uncover executable insights, extensive research, and expert opinions in one place.

Related Content